Management Accounting and Control in Higher Education Institutions: A Systematic Literature Review

1

CEOS.PP—Centre for Organisational and Social Studies of Polytechnic of Porto, Porto Accounting and Business School, Polytechnic Institute of Porto, 4465-004 Porto, Portugal

2

Porto Accounting and Business School, Polytechnic Institute of Porto, 4465-004 Porto, Portugal

3

CETRAD—Centre for Transdisciplinary Development Studies, University of Trás-os-Montes e Alto Douro, 5001-801 Vila Real, Portugal

4

CETRAD—Centre for Transdisciplinary Development Studies, University of Trás-os-Montes e Alto Douro, and NECE-UBI, 5001-801 Vila Real, Portugal

*

Author to whom correspondence should be addressed.

Adm. Sci. 2022, 12(1), 14; https://doi.org/10.3390/admsci12010014

Submission received: 9 December 2021

/

Revised: 11 January 2022

/

Accepted: 13 January 2022

/

Published: 19 January 2022

Abstract

:The new public management reforms have led to significant changes in higher education institutions (HEIs) regarding the management accounting and control (MAC) of these organizations. Therefore, this paper provides an overview of the main studies on MAC in these types of organizations through a systematic literature review (SLR). The PRISMA guidelines were followed, and data were collected from the Web of Science and Scopus databases. The final sample encompassed 50 articles, published between 1981 and 2020. The results show that MAC research tends to focus on management control systems and performance evaluation systems. They also suggest that, although the development and implementation of various MAC tools are crucial for HEIs, such implementation often is partial. This is due to the stakeholders’ perceptions/attitudes regarding the importance of such tools. The results also indicate that institutional theory is the most addressed one. Most of the time, HEIs implement MAC tools due to external pressures. By synthesizing the main trends in MAC, this SLR intends to provide a theoretical contribution to the literature in this research field. Several themes for further research are suggested, such as assessing the relationship between MAC and the management of “knowledge” and intellectual capital in these institutions, and addressing sustainability issues. From a practical viewpoint, HEI managers can obtain important insights to apply the most appropriate tools to their institutions.

1. Introduction

In past decades, accounting ceased to have as its sole purpose the mere registration of financial transactions, becoming a strong tool to, among other things, evaluate organizations’ performance and to maximize their profitability. Management accounting (MA) emerged as a means of responding to the shortcomings of financial accounting, which focuses essentially on controlling and recording relations with third parties, variations in equity and determining the net result in a global context (Hardan and Shatnawi 2013). In the 1980s, Johnson and Kaplan (1987) noted the need for organizations to have a system that could provide information on strategic variables deemed relevant to create value. For example, the Activity-Based Costing (ABC) system, developed by Johnson and Kaplan (1987), emerged as a response to the limitations inherent in the existing systems, which were known for not being timely and rigorous. As for management control, several studies have focused on addressing the deviations between the objectives initially planned and the ones achieved. Once the deviations have been estimated, corrections must be made. In fact, the word “management” refers to an effective manner of using material, human, financial, information and technological resources, which are implemented to address the objectives defined in advance (El Filali and Hassainate 2018). To achieve the desired efficiency and effectiveness, management control systems (MCS) are fundamental. These systems are useful in supporting decision making, such as on changing or maintaining certain organizational activities (Guenther and Schmidt 2015).

According to Pelz (2019, p. 256), “management accounting research has usually focused on large, established companies whose managers use MA to handle organizational complexity”. However, literature is less clear with regard to HEIs. HEIs suffered major changes, namely an increase in their competitive environment due to the Bologna process and public governance since the mid-1980s (Habersam et al. 2013). These facts, along with implementing a European political project for higher education, mass education, less financial resources, and a move to business practices, contributed to developing accounting and accountability in this context (see Boitier and Rivière 2013; Habersam et al. 2013; Hutaibat 2019). The reform process mentioned above greatly affected HEIs, changing the “balance between central governments and academic institutions, increasing the decentralization of responsibilities” (Agasisti et al. 2008) Nowadays, HEIs operate in a competitive market, where the best institutions are those with the best students, teachers and employees, and also the ones that manage to obtain the highest subsidies, whether private or public. Thus, HEIs need to show stakeholders evidence of the accomplishment of their objectives, mission and strategies (Yakhou and Ulshafer 2012). However, according to Jovanović and Dragija (2018), HEI accounting systems are flawed, not allowing managers to make better decisions. There is a lack of knowledge regarding management accounting (including strategic) in these types of organizations (see Hutaibat et al. 2011) where management control systems (MCS) are expected to have a crucial role in their operations, namely regarding performance evaluation and monitoring (El Filali and Hassainate 2018). For example, “many cost saving opportunities have been ignored or lost” (Chang 2013, p. 134). It is a fact that for a long period of time, managers were mainly concerned with HEIs’ economic and financial performance, overlooking long-term consequences (Schaltegger and Zvezdov 2015). Due to the changes mentioned above in the higher education sector in the past decades, it is the authors’ opinion that is important to know the state of the art in management accounting and control in a specific context—the one of HEIs—which also has an important characteristic: the use of knowledge as both input and output. Therefore, this paper aims to provide an overview of the main studies on management accounting and control in HEIs through a systematic literature review (SLR), pointing out some cues for future research. As far as the authors are aware, this is the first SRL addressing this theme in this specific setting. To do so, the following research questions are proposed:

Q1: What are the main themes addressed by studies on management accounting and control in HEIs?

Q2: What are the main results found in studies on management accounting and control in HEIs?

Q3: Which are the main theories addressed by studies on management accounting and control at HEIs?

To answer these questions, this paper examines the results of 50 articles. By reflecting upon what has been done and what needs to be done in the future, this paper contributes to the literature by suggesting new themes to be addressed and different methodologies and contexts to assist researchers in management accounting and control. In practical terms, HEIs’ actors can gain insights on how to manage their organizations better.

2. Theoretical Background

2.1. Management Accounting and Control

According to Shields (2018), two main periods in management accounting and control research can be identified: before and after 1960. In his study, Shields (2018) addressed a large period of time (from 1926 to 2012), aiming to understand how management accounting and control research evolved. The author identified, between 1926 and 1982, six main themes: (1) general literature, including key concepts, information value and the description of practices; (2) estimating the cost of products; (3) cost assignment; (4) cost estimation; (5) decision-making and (6) planning and control (including focused on budgeting, transfer pricing and agency theory). Before the 1960s, the most addressed themes were “product costing, followed by planning and control, decision-making, and description of practice” (Shields 2018, p. 2). Between the 1960s and the 1980s research on product costing and description of practice decreased while planning, control and decision-making were the most researched themes. During the 1970s, management accounting research was greatly influenced by cognitive psychology and agency theory regarding human behavior. Thus, between the 1980s and 2012 the research themes have also changed, with a main focus on planning and control. During this period, research on control has increased, addressing different topics such as performance measurement, incentives or performance evaluation, while topics addressing planning (such as budgeting) have decreased (Shields 2018). Jiang (2019) also conducted a review of articles on management accounting and control, published between 2015 and 2017. The authors considered the following themes as the main ones in research on management accounting and control: (1) management control systems; (2) cost and management accounting; (3) methods for decision-making; (4) general issues in management accounting; (5) externally oriented management accounting; (6) information systems in management accounting and (7) other topics. Researchers such as Shields (2018) and Jiang (2019) claimed that the literature was initially focused on research in cost/management accounting. However, the emphasis shifted to performance evaluation and reward. A similar study was conducted by Xie (2019), who presented a review of the main themes for the same period (2015–2017). The following themes were stressed: performance measurement and evaluation; reward and incentives; and development and integration of management accounting and control systems. Conversely, the least addressed themes were related to cost accounting (namely, ABC) and strategic management accounting. In fact, strategic management accounting research has decreased between 2008 and 2019 (Rashid and McGrath 2020). Hence, it is possible to observe a tendency over time: a decrease of research focused on the traditional cost accounting and an increase in research focused on addressing organizational performance.

2.2. Main Theories Used in Management Accounting and Control Research

With regard to research on management accounting and control, different theories may be applied through multiple perspectives. Each of these theories may provide different answers to distinct problems (Gong and Tse 2009). A sociological theory often referred to in studies on management accounting and control is the institutional theory. According to Al-Htaybat and Alberti-Alhtaybat (2013, p. 14), this theory, pertaining to the domain of organizational and social theories, “has now an established tradition in management accounting research”. For example, Scapens (2012) addressed this theory by analyzing its three facets, namely the new institutional economics (NIE), the new institutional sociology (NIS) and the old institutional economics (OIE). NIE stresses the economic factors that shape the structure of organizations and their management accounting and control practices. However, it is necessary to look beyond economics in order to gain a deeper understanding of all factors that influence organizations. It is this gap that NIS is intended to tackle (Scapens 2012). Initially, NIS tended to emphasize the structural nature of institutions, namely how they are shaped by institutional forces, i.e., forces which are external to organizations. Little emphasis was placed on how institutions are created and how changes occur within them. More recently, NIS has begun to explore the processes that shape practices within organizations. Thus, research drawing on this theory has been addressing the processes by which organizations respond to external institutional pressures. Considering NIE and early NIS research, it can be noted that external pressures can influence the way organizations are structured and managed. While the former explores economic pressures, the latter explores institutional pressures (Scapens 2012). Finally, OIE addresses the different types of economic behavior as well as a potential opportunism. OIE argues that behavior within economic systems (and also within organizations) is embedded in and shaped by institutions. Taken together, the various types of institutional theories have made important contributions to research in management accounting and control, namely regarding processes of change (Scapens 2012). The institutional theory is more commonly used in interpretive studies. Interpretive research aims to better understand and assess practical problems to help researchers explore solutions for such problems (Jansen 2018). Therefore, case studies are more central for interpretive researchers (Jansen 2018).

Other important theories are addressed in management accounting and control, such as: contingency theory, agency theory, sociological theories (which include the institutional theory) and psychological theories (Gong and Tse 2009). Regarding these theories, contingency theory should be stressed. The adoption of contingency theory in accounting system emerges due to contradictory results which cannot be solved by the existent universal framework. This theory is important for the process of adjusting a particular management practice to the variables related to a specific organization. Factors such as technology, organizational structure and the environment have been invoked to explain why accounting systems differ from one situation to another (Gong and Tse 2009; Abba et al. 2018). According to Al-Htaybat and Alberti-Alhtaybat (2013, p. 14), “contingency theory is still one of the most popular research approaches in management accounting”. This theory is commonly used in more positivist contexts (Al-Htaybat and Alberti-Alhtaybat 2013). Positivist researchers see case studies as exploratory, aiming to develop a hypothesis to be tested through quantitative methodologies.

Finally, most studies on management accounting and control involving the agency theory are based on the principal–agent model, which assumes that individuals can anticipate all possible future contingencies. In such cases, management accounting systems can be used by principals to align agents’ interests with their own (Gong and Tse 2009). As for the sociological theories which, as mentioned above, include the institutional theory, they focus on how organizations are established through interactions between humans, organizations and society. These theories consider that management accounting and control systems are social practices, rather than mere techniques for internal decision-making and organizational efficiency (Gong and Tse 2009). Finally, psychological theories can also be emphasized. These theories are applied in management accounting and control research to examine relationships between individual behavior and management accounting and control practices (Gong and Tse 2009). Hiebl (2014) addressed an example of a psychological theory called the upper echelons theory. This theory follows the premise that the demographic characteristics (age, gender, education and tenure) of top managers have an influence on their strategic choices, which in turn influences the organizations’ results. Most studies in this field of research make use of the above theories (see Rashid and McGrath 2020).

3. Methodology

In this paper a systematic literature review (SLR) is conducted and applied to higher education institutions (HEIs), considering that the methods used in traditional reviews do not clearly identify what is or is not known about a given theme. SLRs differ from traditional narrative reviews by adopting a scientific, replicable process, meant to minimize errors or biases through exhaustive literature searches (Tranfield et al. 2003).

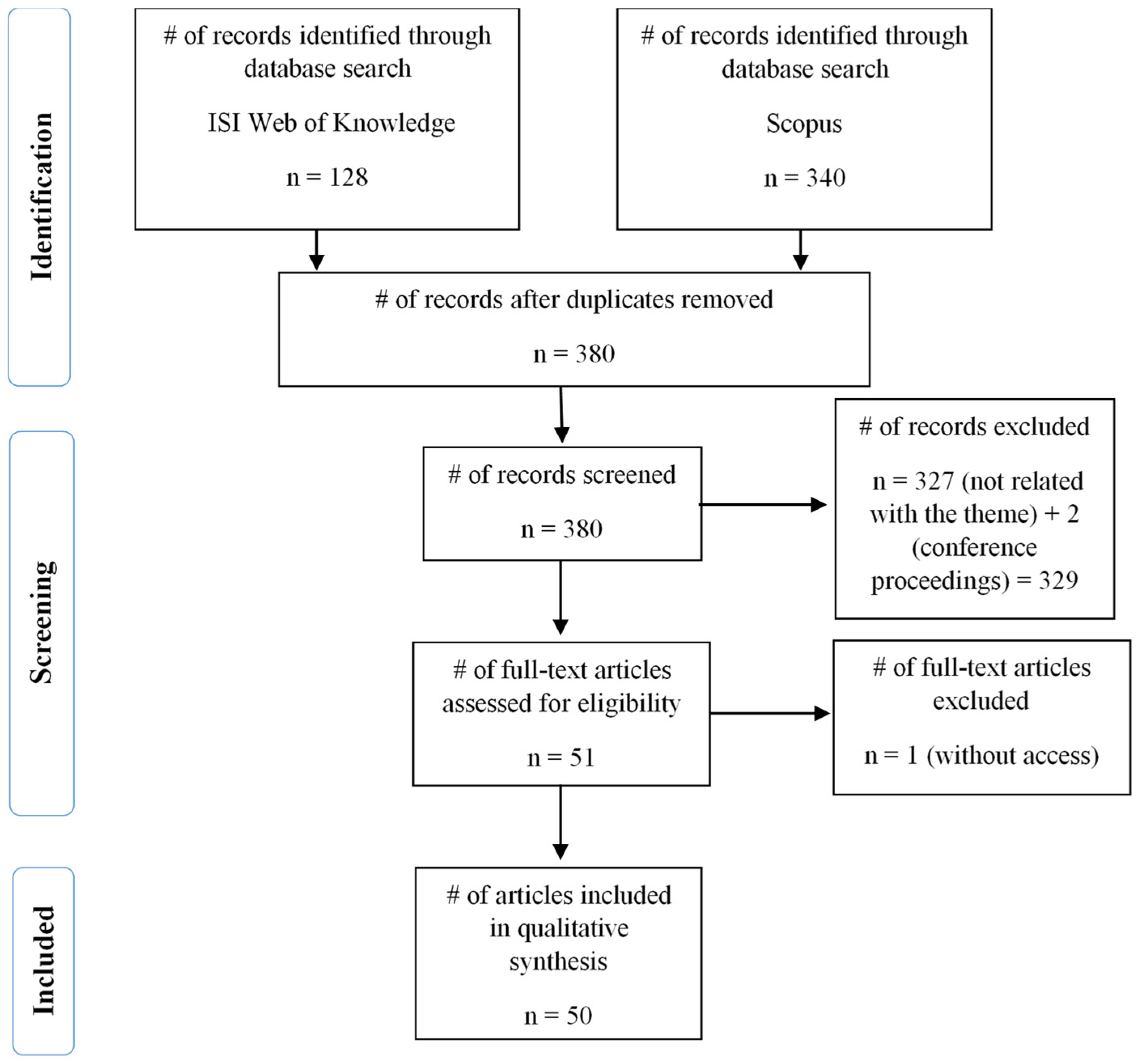

In order to select the sample for the present study, the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analyses) guidelines, originally proposed by Liberati et al. (2009) and updated in 2020 (see Page et al. 2021) were followed. The 2020 PRISMA flow diagram is based on three steps: identification, screening and included articles (see Figure 1).

Thus, we started by choosing the databases in order to collect the articles to be included in the RSL. The chosen databases were Web of Science and Scopus, which is justified by them containing a predominance of publications with high scientific recognition. Data were collected on 27 June 2020 and the same protocol was applied to both databases. First, a search for publications was conducted using the following keywords: “management account*” or “management control”, and “higher educat*” or “universit*” or “HEI” (higher education institution) or “HEO” (higher education organization) to specify the context. A total of 844 results was attained: 258 from the Web of Science database and 586 from Scopus. Then, a filter by research field was applied, considering the topic and context of application. In the Web of Science, the following domains were selected: business finance; educational research; management; business; education scientific disciplines; economics; interdisciplinary social sciences; public administration and multidisciplinary sciences. After applying the filter, the sample was narrowed to 196 results. Regarding the Scopus database, the following domains were selected: business management and accounting; social sciences; economics, econometrics and finance, and decision sciences. Consequently, the sample decreased to 411 articles. Finally, it was decided to select only scientific articles, reviews and early access articles, excluding other publications such as books, conference proceedings and the so-called gray literature. It was also decided not to impose any type of time restriction. The sample was then narrowed to 128 articles collected from Web of Science and 340 articles collected from Scopus. Finally, duplicates were eliminated (88 articles). Considering both databases, a sample of 468 results was obtained, thus concluding the first stage of PRISMA (identifying the publications to assess). In the screening stage, the titles, abstracts and keywords of the remaining 380 articles were read, which led to the exclusion of 329 documents (327 were not related to the theme and 2 were “conference reports”). Consequently, 51 articles were considered eligible for analysis. However, 1 article was excluded due to inaccessibility reasons, resulting in a final sample of 50 articles. In order to structure the articles’ analysis, an Excel database was created in which relevant information was included for each article.

4. Results

This section is devoted to the qualitative analysis of selected articles, highlighting their contents and bibliometric features.

4.1. Main Topics Addressed in Studies on Management Accounting and Control in HEIs

HEIs pertain to a sector that has been experiencing considerable changes through the reforms of the new public management (NPM). In fact, during the assessment of the sample, a category emerged, encompassing several articles focused on “NPM reforms and changes in HEIs”, through management control systems (MCS) or performance evaluation systems (see Sizer 1981; Petrides et al. 2004; Chung et al. 2009; Boitier and Rivière 2013, 2016; Martin-Sardesai 2016; Visser 2016; Martin-Sardesai et al. 2019; Kallio et al. 2020).

With regard to NPM reforms, Kallio et al.’s (2020) study aimed to understand how public sector reforms have affected the organizing of HEIs in Finland, the performance evaluation criteria and ultimately their raison d’être. On the other hand, Boitier and Rivière (2016) studied how MCS can be drivers of a new management logic in a French university, considering a context where strong institutional logic prevails. Regarding changes in HEIs, Martin-Sardesai (2016) conducted a study that aimed to explore how MCS complement institutional entrepreneurship. Similarly, Agyemang and Broadbent (2015) examined how HEIs in the UK developed MCS in response to external impositions.

The results also suggest that some articles focus their themes on another category: cost/management accounting (see Laitinen 2003; Modell 2006; Kont and Jantson 2011; Palowski 2011; Acevedo et al. 2014; Molina-Sanchez et al. 2019; Hutaibat and Alhatabat 2020). Brusca et al. (2019) studied the changes and benefits of implementing cost accounting in Spanish universities. Hutaibat and Alhatabat (2020) explored the extent and determinants of the adoption of management accounting practices in universities in the United Kingdom. Palowski (2011) studied the development of management accounting (more specifically, the ABC model) in universities in the United Kingdom, a study similar to that of Hutaibat and Alhatabat (2020). Sánchez et al. (2019) also explored the ABC, proposing an activity-based management model in order to calculate the costs of different departments of a Spanish university. Regarding ABC, Kont and Jantson (2011) addressed the ABC and time-driven activity-based costing (TDABC) methods in the context of a university library, focusing on the strengths and weaknesses of both methods to determine which of the two would be more suitable for such a particular case.

Several articles address “strategic management accounting” (see Agasisti et al. 2008; Hutaibat et al. 2011; Hutaibat 2019; Marlina et al. 2020; Huerta-Riveros et al. 2020). Hutaibat et al. (2011) explored the concept of strategic accounting in an English university, analyzing the practices and processes of strategic management accounting, as well as the meaning attributed by the actors. Hutaibat (2019), based on Bourdieu’s theory of practice, presented the results of a study on the higher education sector in Jordan, in which he researched strategic accounting, accounting for strategic management and power structures. Finally, it is important to highlight Marlina and Tjahjadi’s (2020) critical review and synthesis about the relationship between strategic management accounting and the performance of universities.

Other articles focus on management control/management control tools (see Tsamenyi et al. 2008; Broadbent 2010; Küpper 2013; Ahrens and Khalifa 2015). For example, Ahrens and Khalifa (2015) sought to understand the impact of regulation on management control practices in three United Arab Emirates universities. The authors explored how certain organizational controls are adapted to HEIs’ contexts, supporting their routines. Another example comes from Tsamenyi et al.’s (2008) study, which sought to understand the nature and dynamics of management control in a private family-owned university in Indonesia.

The analysis of the articles also allowed us to identify a category concerning the “stakeholders”, and their perceptions and attitudes towards MCS, performance evaluation systems and strategic management tools. The actors’ motivation is also addressed, as well as how such motivation is affected (or not) by the excessive control and pressure exerted in HEIs. Actors’ characteristics and their influence on the use of the aforementioned systems are also stressed (see Habersam et al. 2013; Minelli et al. 2015; Sutton and Brown 2016; Bollecker 2016; Jacomossi and da Silva 2016; Dobija et al. 2019; Pilonato and Monfardini 2020; Bobe and Kober 2020; Heinicke and Guenther 2020).

Regarding perceptions, Heinicke and Guenther (2020) analyzed the mediating role of MCS in three German universities, as well as deans’ and senior managers’ perceptions on the role of management control mechanisms in such institutions. Pilonato and Monfardini (2020) assessed the perceptions of course directors and teaching managers regarding the introduction of a new performance evaluation system in Italian universities. Similarly, Dobija et al. (2019) aimed to observe how performance evaluation is perceived by deans, researchers and teaching oriented in the Polish university context. As for attitudes, Bollecker (2016) analyzed how the adoption of management accounting is influenced by different stakeholder groups of a French university. Regarding the motivation of different academic actors, Sutton and Brown (2016) sought to understand how HEIs carry out management control without influencing the motivation of the different academic actors. Finally, Bobe and Kober (2020), based on the upper echelons theory, analyzed how the demographic characteristics of 39 Australian public universities’ deans were related to the use of MCS, as well as financial and non-financial performance measures in these institutions.

Another category refers to “budgeting” (see Jones et al. 1986; Ozdil and Hoque 2017; Kenno and Sainty 2017). For example, Kenno and Sainty (2017) reviewed the challenges of implementing a new activity-based budgeting model through a case study at a Canadian university. Ozdil and Hoque (2017) presented the results of a case study on the implementation of a new budgeting model at an Australian university.

Other articles address “quality management in HEIs”. Regarding this theme, Van Kemenade et al. (2008) developed a new concept of quality in HEIs, following the premise that although multiple definitions of quality do exist, there is a need for a new definition to explain recent questions regarding quality in higher education. del Pino et al. (2018) also developed a methodology to diagnose the predominant cultural conditions in a university in Ecuador and determine the type of change that needs to be applied, so as to support the development of quality management systems in higher education.

In addition to the aforementioned themes, some articles also address “sustainability, social responsibility and environmental management” (see Sulaiman and Rahman 2013; Chang 2013; Wigmore-Álvarez and Ruiz-Lozano 2014; Arroyo 2017). Sulaiman and Rahman (2013) addressed a university’s community awareness regarding environmental issues and environmental management accounting and to what extent such a community is aware of the need for information on environmental costs. Chang (2013) focused on the management of environmental costs through an accounting perspective, by researching costs management practices concerning electricity, water and paper consumption, as well as waste generation.

Finally, a last category named “financial disclosure” was identified, encompassing only one article: the one by Jovanović and Dragija (2018), in which the financial reporting systems of two universities are assessed at a micro and macro level, the former referring to management accounting and the latter to a public policy framework.

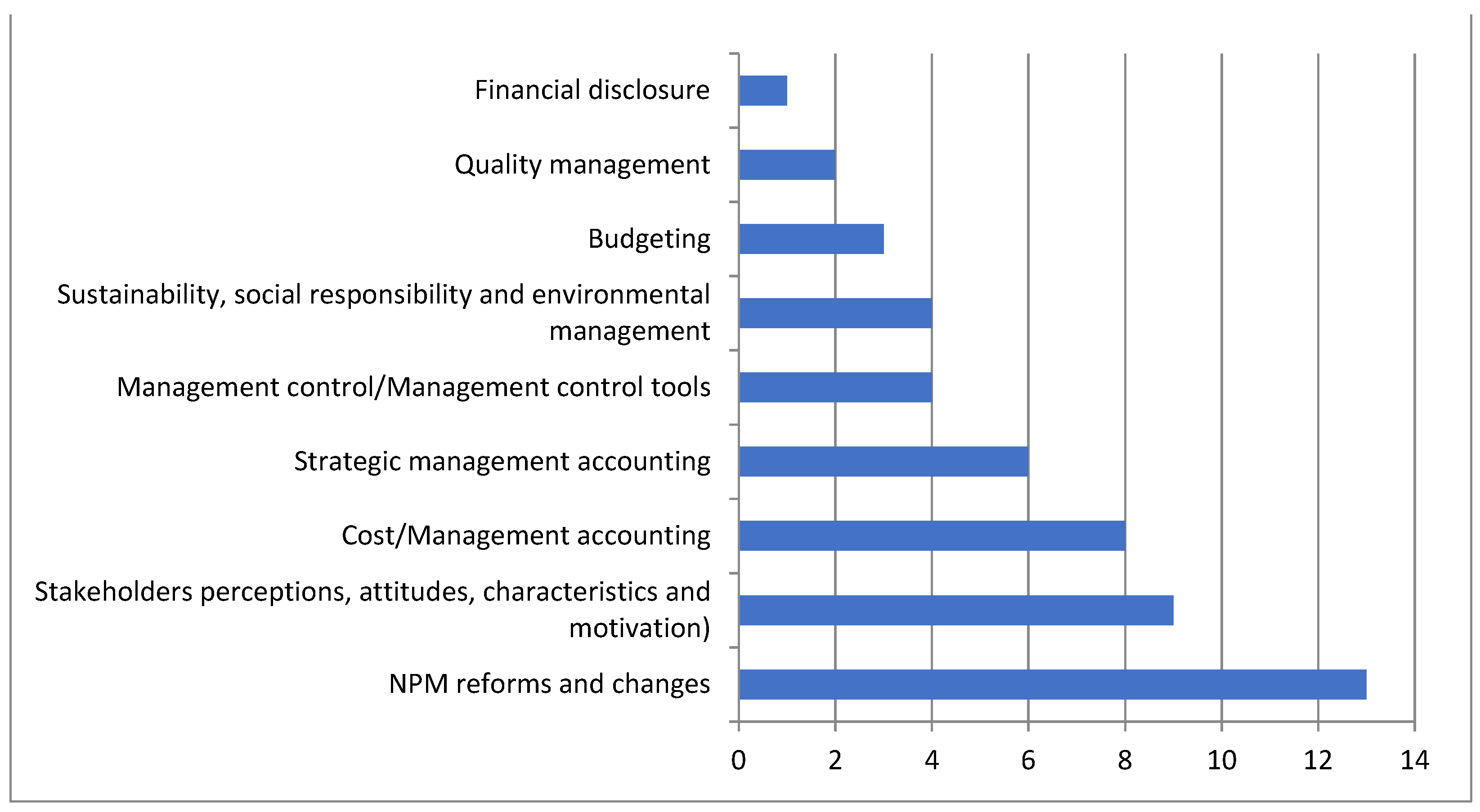

In summary, it was possible to group the topics addressed in the sample under each of the following categories: (1) NPM reforms and changes in HEIs (through MCS or performance evaluation systems); (2) cost/management accounting; (3) strategic management accounting; (4) management control/management control tools; (5) stakeholders (perceptions, attitudes, motivation and characteristics); (6) budget; (7) quality management; (8) sustainability, social responsibility and environmental management; and (9) financial disclosure.

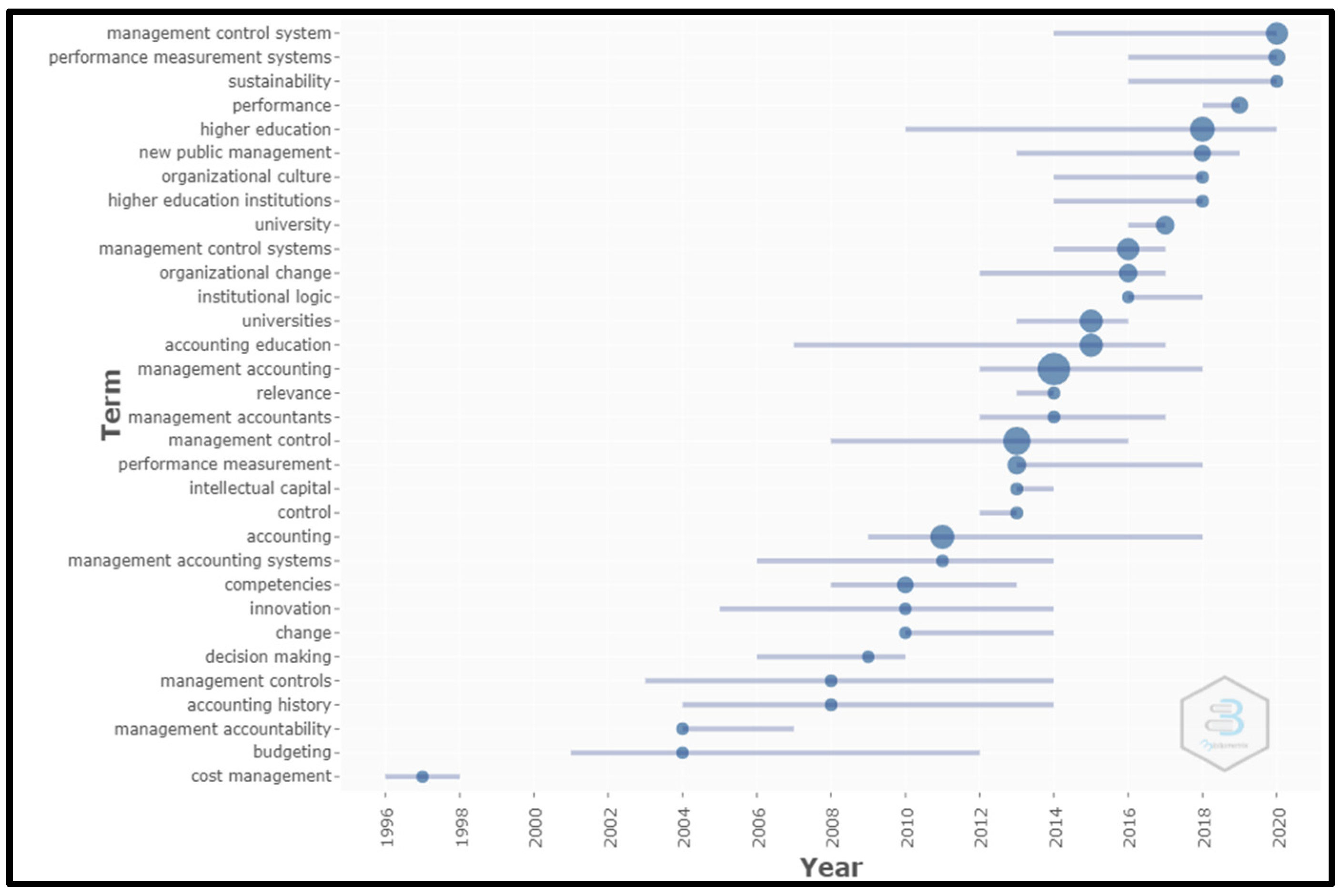

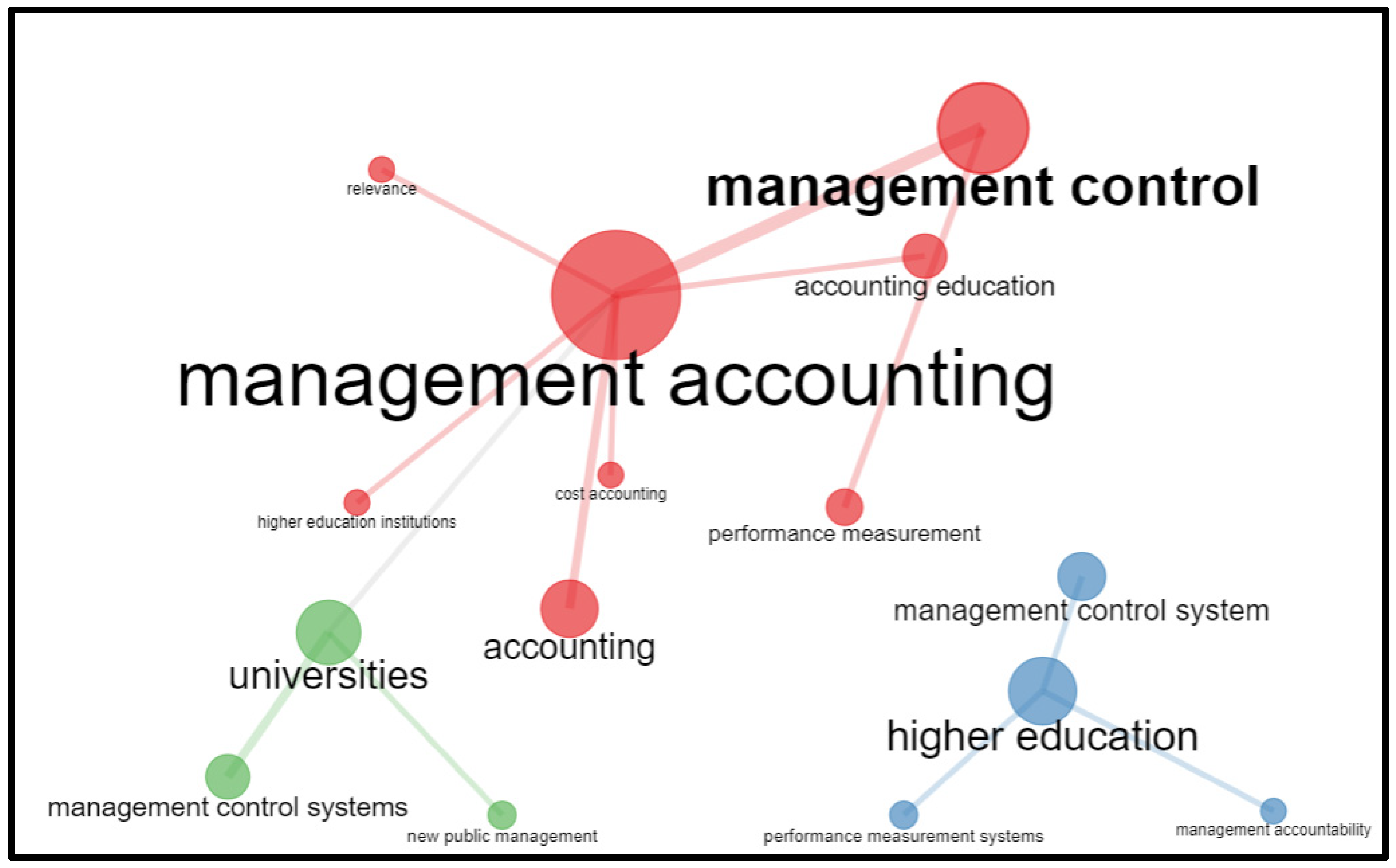

Next, a longitudinal perspective regarding the evolution of the themes of the articles comprising the sample is presented (see Figure 2), as well as the co-occurrence networks (see Figure 3).

Longitudinal Perspective

The articles encompassing the sample were published between 1996 and 2020. To assess the evolution of the themes in a longitudinal stance, four periods were considered: 1996–2005; 2006–2010; 2011–2015; 2016–2020.

The first period, ranging from 1996 to 2005, is the one with the least number of articles published (4 articles), although the longest (24 years). Two articles refer to NPM reforms and changes in HEIs (through MCS or performance evaluation systems), one article is about budget and another about cost/management accounting. Between 2006 and 2010, 7 articles were published. Two articles refer to NPM reforms and changes in HEIs and two others address themes concerning management control/management control tools. Finally, one article was published regarding each of the following categories: strategic management accounting, quality management and cost/management accounting. In a third period (2011 to 2015), 14 articles were published. Of these, 3 articles addressed NPM reforms and changes in HEIs, sustainability, social responsibility and environmental management, and cost/management accounting, respectively. Two articles were about management control/management control tools and another two about stakeholders’ perceptions, attitudes, characteristics and motivation towards MCS, performance evaluation systems and strategic management tools. Finally, only one article was published on strategic management accounting. In the last period (2016 to 2020), 25 articles were published. The most covered themes relate to stakeholders (7 articles) and NPM reforms and changes in HEIs (6 articles). It should also be stressed that the only article pertaining to the category “financial disclosure” was published during this period.

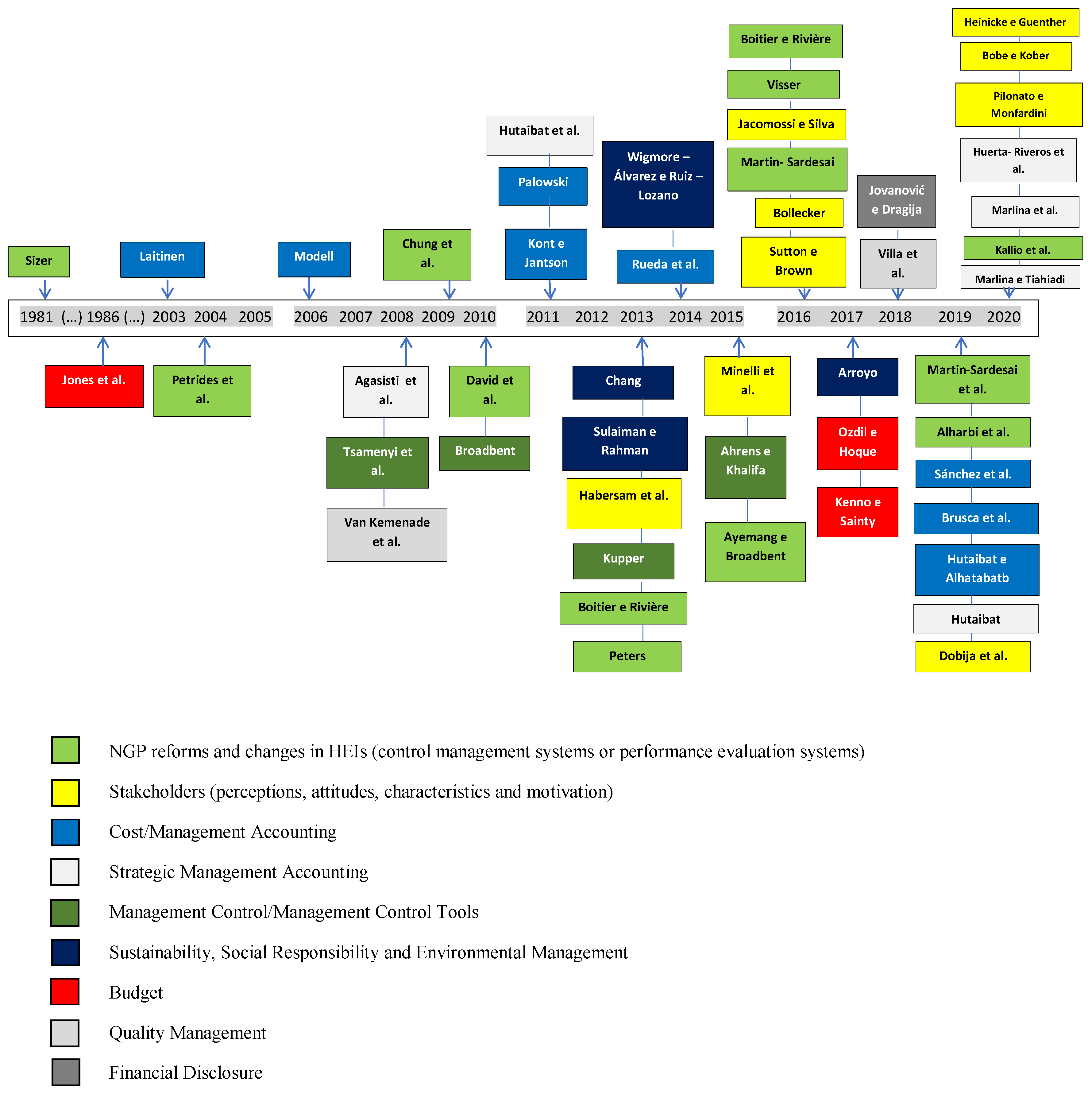

Throughout the 39 years in which the articles in the sample were published, there are two themes that are common to all stages: NPM reforms and changes in HEIs and cost/management accounting (see Appendix A). The largest number of articles published over time relates to NPM reforms and changes in HEIs (13 articles, representing 26% of the sample), with 8 being published between 2011 and 2020 (see Figure 4). Furthermore, 8 articles on costs/management were published, 6 of them between 2011 and 2020. Regarding strategic management accounting, 6 articles were published between 2006 and 2020, with 4 articles being published between 2016 and 2020. In fact, 50% of the sample was published between 2016 and 2020. The remaining categories were published between 2013 and 2020. It is also important to stress that the most recent articles pertain to the “strategic management tools” and the “sustainability, social responsibility and environmental management” categories. Additionally, the themes regarding stakeholders are the most frequent ones in articles published between 2016 and 2020 (7 articles published during this period).

In summary, the longitudinal analysis suggests that studies on management accounting and control in HEIs tend to focus on MCS and performance evaluation systems, whether they are related to NPM reforms and changes in HEIs or the stakeholders’ perceptions and attitudes. Conversely, the least addressed topics in the sample are those included in the following categories: management control/management control tools (4 published articles), sustainability, social responsibility and environmental management (4 published articles), budget (3 published articles), quality management (2 published articles) and financial disclosure (1 article).

4.2. Main Results of Studies on Management Accounting and Control in HEIs

The categories highlighted in the first research question were adopted to describe the articles’ results. Some articles are used to illustrate examples of such results for each category.

Regarding NPM reforms, Kallio et al. (2020) suggested that reforms in Finland’s HEIs led to changes in administrative structures, planning and control systems, staff coordination and roles, and power allocation which became a challenge for these institutions. Boitier and Rivière (2016) suggest that combining different management logics within that institution and a fragmented implementation of a new management logic were possible issues. This is explained by the fact that different actors, namely, administrators, politicians and academics, adopt these logics in different ways and according to their roles, which is also affected by their professional trajectory and the connections they maintain outside the university. When referring to changes in HEIs, Martin-Sardesai (2016) found that institutional entrepreneurship and MCS complement each other. Agyemang and Broadbent (2015) considered that internal MCS developed by HEIs in the United Kingdom are in accordance with the Research Excellence Framework. Although these systems are accepted by these institutions, they partly encourage a deviation from the values hitherto held by these institutions.

Regarding the articles addressing cost accounting/management, Brusca et al. (2019) observed that in recent years many Spanish universities have made great efforts to implement a cost accounting system, largely due to the requirements of the central government. Nevertheless, the results suggest that universities tend to emphasize cost accounting for accountability purposes. Hutaibat and Alhatabat (2020) studied the adoption of management accounting practices in United Kingdom universities, suggesting that larger universities adopt these practices more frequently when compared with smaller ones. They justify this by arguing that larger universities need more refined tools to better manage their many functions. Some articles under this category mention the adoption of the ABC (see Palowski 2011; Kont and Jantson 2011; Sánchez et al. 2019). Palowski (2011) found that the implementation of a costing system in a UK HEI was based on misunderstandings of several key aspects of the ABC theory, namely related to resource and activity costs. Sánchez et al. (2019) suggested that ABC allows HEIs to identify activities that do not add value, also assessing how they can be eliminated or, if not possible, how resource consumption can be reduced. Finally, Kont and Jantson (2011) argued that both ABC and TDABC can be applied in university libraries.

When referring to management accounting, several articles address it as a strategic management tool. Three articles are presented to illustrate this approach. Hutaibat (2019) reached similar results, suggesting that strategic management accounting can be regarded as having different degrees, and that the mindset determines how accounting is perceived by the different actors. Similarly, Hutaibat et al. (2011) suggest that strategic management accounting is dealt with and the perceptions of institutional members are shaped according to each individual’s mindset (whether bureaucratic or entrepreneurial). Finally, Marlina and Tjahjadi (2020) aimed to understand, through a critical review, how strategic management accounting increases university performance. The results reveal that knowledge is still limited in this field.

A fourth category addresses management control/management control tools. Two articles are provided as illustrations. Ahrens and Khalifa’s (2015) study suggests that the compliance with regulated management control in three universities in UAE is nothing more than a creative process of organizing and translating general prescriptions and applying them to a specific context. Tsamenyi et al.’s (2008) study considers that cultural factors impact management control practices in less developed countries such as Indonesia.

A fifth category refers to stakeholders’ perceptions, attitudes, characteristics and motivation towards MCSs, performance evaluation systems and strategic management tools. Regarding perceptions/attitudes, Heinicke and Guenther (2020) found significant differences between top managers and deans of three German universities regarding the relationship between structural autonomy and management control, and between management control and teaching and research performance. Top managers only consider strategic boundaries and beliefs as significantly related to teaching performance, whereas, for deans, more autonomy is related to more emphasis on MCS. Pilonato and Monfardini (2020) found that teaching managers and course directors at two Italian universities have different perceptions regarding performance evaluation systems. Teaching managers have a more positive view, while course directors tend to be more cautious and sceptical, as they see reforms as problematic and inconsistent due to the length of procedures and the restrictions on their freedom to manage. Finally, Dobija et al. (2019) found that the use of performance evaluation depends on both exogenous factors and endogenous factors. At the internal level it is possible to verify different attitudes of deans, researchers and teaching staff, and even some resistance to the use of performance evaluation.

Regarding the stakeholders’ attitudes towards control systems, Bollecker (2016) found that different actors (financial director, three vice-presidents of three different departments and the director of general services) have different attitudes towards the adoption of total costing tools. These differences are explained by discrepancies in resource allocation and availability, reallocation strategies, and by reasons related to the institution’s history. With respect to stakeholders’ motivation, Sutton and Brown (2016) showed that the design and operationalization of an MCS appeared to maintain and even increase the motivation of the different academic actors. This was due to the fact of being under the illusion that no or very little control was being exercised. Finally, with regard to stakeholders’ characteristics, Bobe and Kober (2020), through their study of 39 Australian public universities, considered that deans’ personal characteristics are related to the importance they place on financial and non-financial performance measures, as well as how they use MCS.

The “budget” category is exemplified by Kenno and Sainty (2017) and Ozdil and Hoque (2017) studies. Regarding the first article, the authors described the difficulty of implementing a new budgeting system in a Canadian university, due to several issues such as the implementation complexity or problems related to the maintenance of key personnel. Regarding the second one, it was concluded that the change process of an Australian university was dependent on the chosen budget model.

As for quality management, Van Kemenade et al. (2008) found that the lack of acceptance of external evaluation systems in higher education may be associated with too much control and too little improvement. del Pino et al. (2018) claimed that the application of a quality management system at a university in Ecuador was feasible although cultural and sociotechnical barriers were experienced, thus preventing the achievement of predefined quality standards. Nevertheless, improvement plans were subsequently implemented resulting in an increase of the commitment and participation level of those involved which, consequently, resulted in better outcomes.

Regarding the category encompassing articles on sustainability, social responsibility and environmental management, two articles were analyzed. On the one hand, Sulaiman and Rahman (2013) concluded that staff consider information on environmental costs as useful for managing the impact of their activities on the environment. On the other hand, Chang (2013) found that knowledge about environmental management accounting, in three universities under study, is limited and that efforts to improve environmental performance, particularly from an accounting perspective, are scarce.

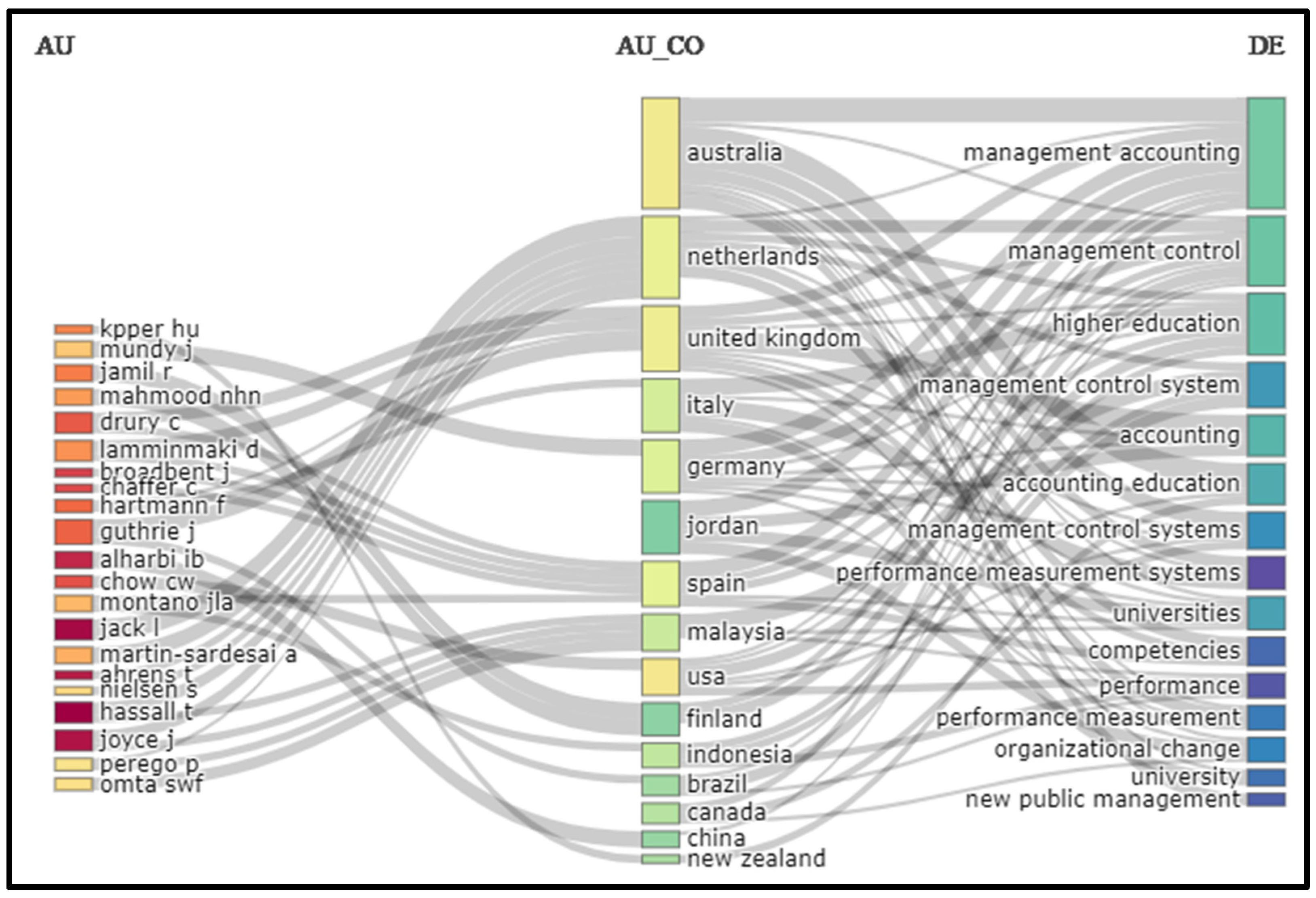

In the final category, labeled “financial disclosure”, the article by Jovanović and Dragija (2018) shows that the existence of financial reporting systems in the two universities under study is particularly useful for the decision-making process. The authors also suggested that the accounting function in HEIs is undervalued, since it is usually used for reporting purposes. Figure 5 below portrays the most relevant authors (AU), countries (AU_CO) and research topics (DE).

4.3. Thematic Evolution

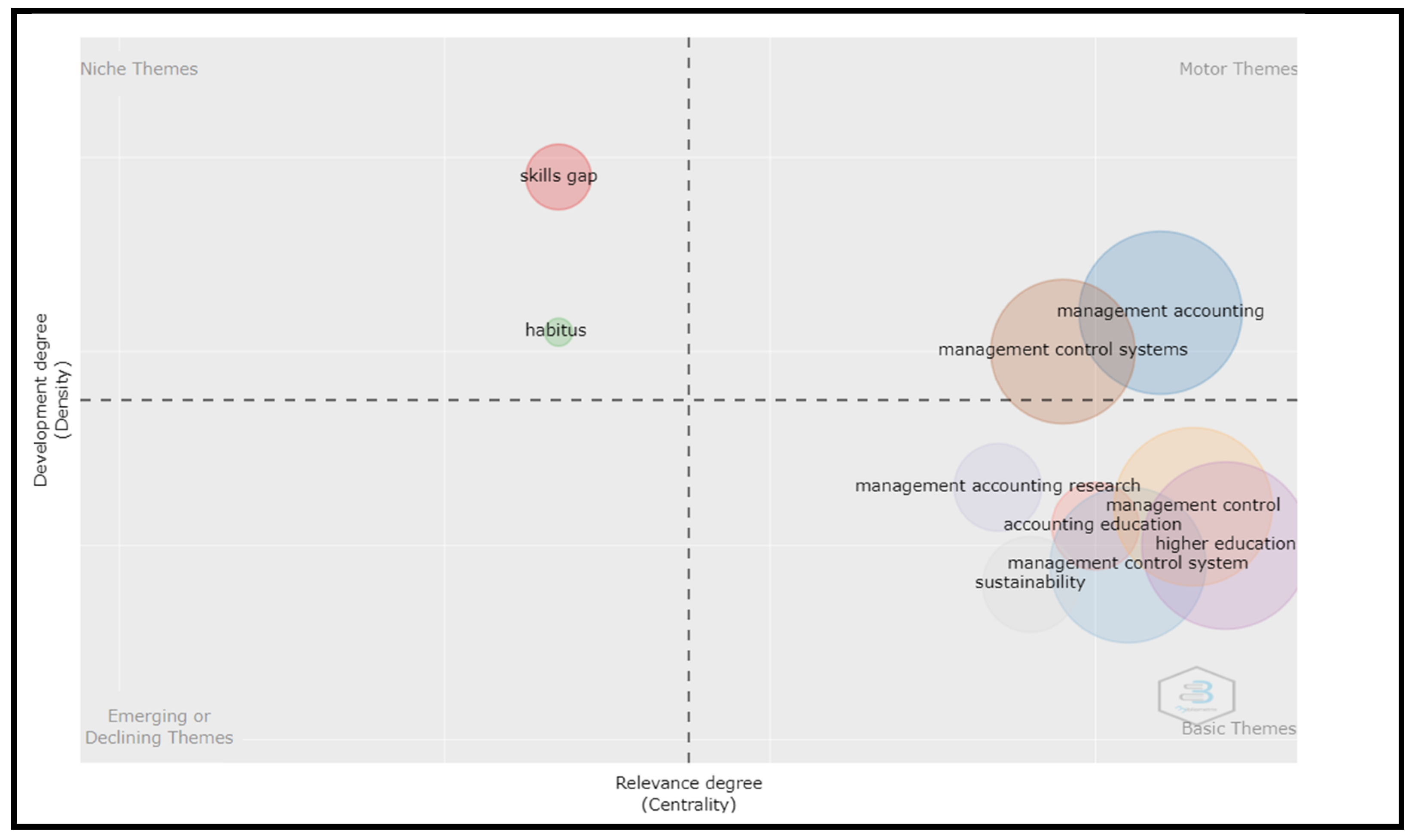

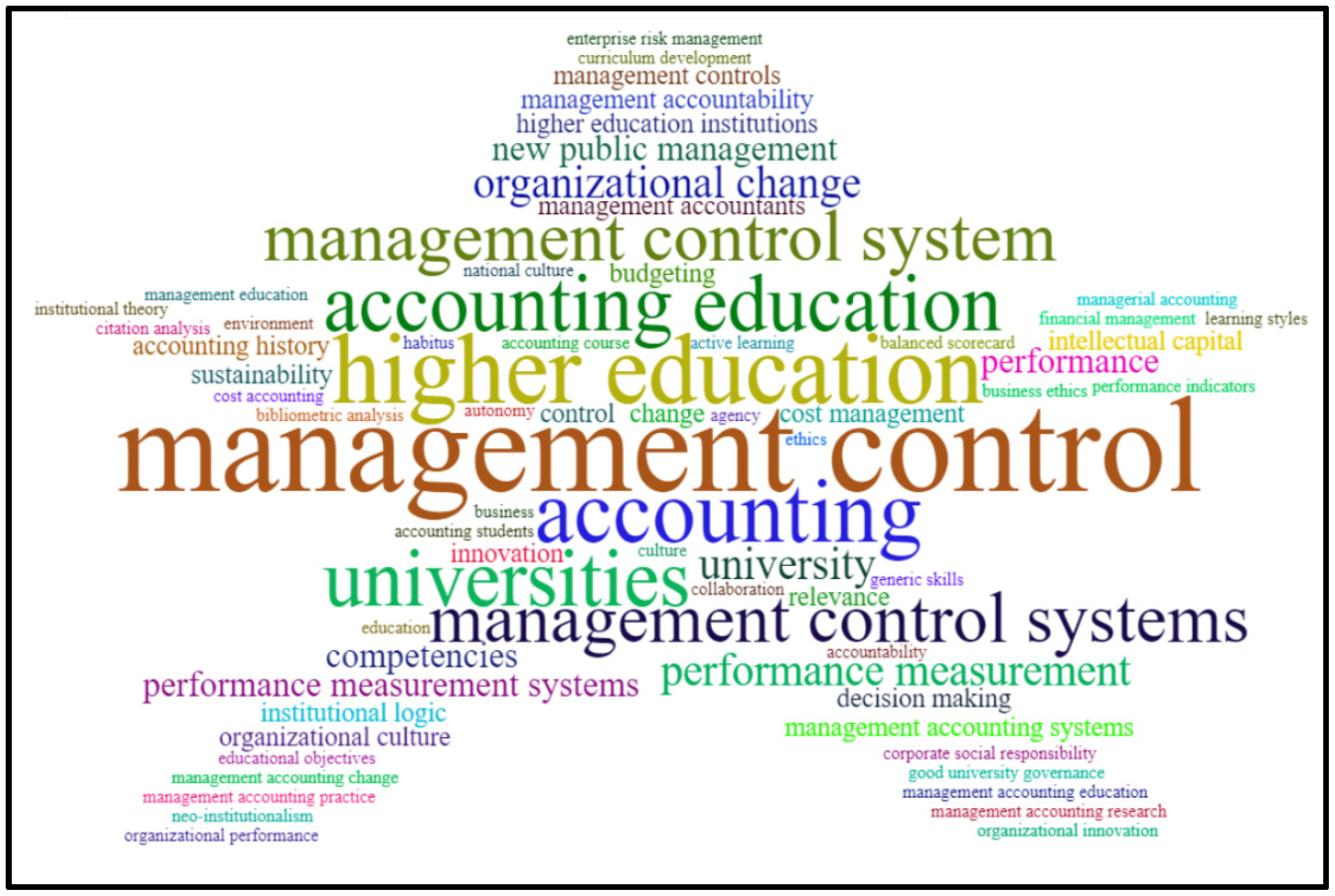

Academic research’s leading theoretical and conceptual research themes on management accounting and control in HEIs can be divided into four quadrants, which are detailed in Figure 6 below. It is possible to observe that research in this area is grouped into “motor themes” and “basic themes”. The engine themes drive the research, and they are the major research areas from which the remaining research begins. This quadrant encompasses management accounting and management control systems. The lower right quadrant depicts the “basic themes”, which are the most explored ones. This quadrant presents themes related to higher education, accounting education, management control and sustainability. Figure 7 shows the main themes which have been stressed in this field of research throughout the period under analysis.

4.4. Main Theories Addressed in Studies on Management Accounting and Control in HEIs

Through the analysis of the articles that comprise the sample it was possible to identify 15 articles addressing theories. Thirteen different theories are mentioned (see Table 1):

The most addressed theory is the institutional theory and its respective approaches—new institutional economics (NIE), new institutional sociology (NIS) and old institutional economics (OIE)—referred to in 7 articles. The isomorphism theory is addressed in 4 articles, and Bourdieu’s theory of practice and the grounded theory are mentioned in 2 articles each. The remaining theories appear in a single article (see Table 1). Regarding the aforementioned theories, it is possible to conclude that most of them are sociological and psychological ones. With regard to sociological theories, the institutional theory, Bourdieu’s theory of practice, the theory of rational choice, the so-called negotiated order and the isomorphism theory stand out. The psychological theories encompass the higher-ranking theory, self-determination theory, self-referential theory and professionalism theory. A total of 9 theories (out of the 13 theories identified) fall into this typology.

5. Some Reflections for Further Research and Concluding Remarks

The results of the first research question—what are the main topics covered in the studies on management accounting and control in HEIs—allowed us to identify nine categories, each one encompassing articles with similar themes. The identified categories were labeled: (1) NPM reforms and changes in HEIs (through MCS or performance evaluation systems); (2) cost/management accounting; (3) strategic management accounting; (4) management control/management control tools; (5) stakeholders (perceptions, attitudes, motivation and characteristics); (6) budgeting; (7) quality management; (8) sustainability, social responsibility and environmental management; and (9) financial disclosure. These themes are aligned with the ones adopted by management accounting and control in other settings, both directly or indirectly. Directly, cost/management accounting, strategic management accounting, and management control/management control tools are all themes researched since the 1960s, and mainly since the 1980s (see Shields 2018; Jiang 2019; Xie 2019). Themes of financial disclosure and sustainability are more recently found in the literature. Indirectly, management accounting and control is also present in studies which address NPM reforms and changes in HEIs. However, in these cases, some articles focus on NPM as, for example, drivers of management accounting and control change (e.g., according to Kallio et al. (2020), NPM reforms in Finland led to several changes such as in planning and control systems). Regarding the theme “stakeholders”, management accounting is, according to Shields (2018, p. 3), “about more than just numbers: it is also about people and how they make decisions, are motivated, and interact with others”. Budgeting and quality management can be considered part of a broader theme, which Shields (2018) entitled “planning and control”.

Furthermore, a longitudinal analysis of these categories allowed us to understand their evolution between 1981 and 2020. More specifically, it was found that most articles address NPM reforms and changes in HEIs (through MCS or performance assessment systems). The 13 articles which focus on this theme are also transversal to the four time periods which were previously defined, although 8 were published between 2011 and 2020. These facts are in line with the work of Funck and Karlsson (2020), who argue that NPM has been a major focus of debate since its inception, continuing nowadays to capture attention, also stressing the role of accounting.

Another category which encompasses articles published during all the four time periods is the one named “cost/management accounting”. Furthermore, only the category “strategic management accounting” includes articles published (6 articles) in three of the identified periods (the remaining categories comprise articles published in only two periods); more specifically, between 2006 and 2020. Nevertheless, most of the articles addressing topics related to strategic management accounting were published between 2016 and 2020. Once again, it should be stressed that 50% of the sample (25 articles) was published between 2016 and 2020.

The themes regarding the “stakeholders”, “strategic management accounting” and “sustainability, social responsibility and environmental management” are the most recent ones. The articles referring to the perceptions, attitudes, motivation and characteristics of stakeholders were published between 2013 and 2020 (9 articles) while the articles on sustainability, social responsibility and environmental management were published between 2013 and 2017 (4 articles). Despite the fact that the topics on stakeholders have emerged not so long ago, these topics are the ones on which research on management accounting and control in HEIs was most active in the period ranging from 2016 to 2020. Furthermore, the themes least often addressed throughout the sample are those in the following categories: management control/management control tools; sustainability, social responsibility and environmental management; budget; quality management; and financial disclosure.

In summary, it can be observed that 39 out of 50 articles were published in the past decade. That is why the literature on management accounting and control in HEIs is dispersed, i.e., it does not follow the general literature as a whole. Instead, a general literature has evolved over a much larger period, providing the basis for more specific settings such as HEIs. Changes occurred during the 1980s led to an increase in the importance of themes related to planning and control and stressed the importance of performance (see Shields 2018). During this period, research on control has increased, addressing different topics such as performance measurement, incentives and performance evaluation, while topics addressing planning (such as budgeting) have decreased (see, for example, Shields 2018; Xie 2019).

Some similarities can be found when comparing management accounting and control in broader terms (see Section 2) with management accounting and control in HEI. On the one hand, Shields (2018) stated that studies on management accounting and control, which initially (between 1926 and 1986) were focused on costs, progressively shifted their focus to performance measurement and reward (mainly between 2015 and 2017). Jiang (2019) and Xie (2019) reported similar results. Xie (2019) found that 54% of his sample addressed MCS, stressing the following sub-themes: performance measurement and evaluation; reward and incentives; development and integration of management accounting and control systems. On the other hand, the results for the first research question allow us to conclude that research in this area has become interested in topics related to stakeholders’ perceptions, attitudes, characteristics and motivation towards MCS, to performance evaluation systems and strategic management tools, as well as to the NPM reforms and changes in HEIs (through MCS or performance evaluation systems). These themes, in addition to being the most addressed themes throughout the sample, are also the ones that are prevalent in the articles published between 2016 and 2020. In short, based on these results, we can claim that management accounting and control research in HEIs tends to focus on themes related to MCS and performance evaluation systems, following a more general literature. Furthermore, our findings also suggest an increase in strategic management accounting research, differing from Rashid and McGrath’s (2020) findings. In light of these findings, it is the authors’ opinion that future research on management accounting and control in HEIs should go back to basics, i.e., it should emphasize cost accounting and service costing. Only one article mentioned cost accounting: that of Sánchez et al. (2019), which suggested a model (based on activity-based costing) for calculating the costs of different departments in a public university.

Regarding the second research question, the following conclusions can be drawn: MCS and performance evaluation systems are seen as a viable and successful option to be developed and implemented by HEIs. However, it should be stressed that not all academic actors perceive these changes in the same way, something that often leads to partial implementation of these systems (see Kallio et al. 2020; Boitier and Rivière 2016; Martin-Sardesai 2016; Agyemang and Broadbent 2015). In fact, strategic beliefs and structural autonomy are related to the emphasis that senior managers and deans place on MCS (Heinicke and Guenther 2020). Additionally, stakeholders’ demographic characteristics can have an influence on the importance they place on financial and non-financial performance measures, including MCS (Bobe and Kober 2020). In fact, academic stakeholders may have different perceptions and attitudes towards MCS and performance measurement systems, something which can potentially lead to resistance to adopting such systems (Pilonato and Monfardini 2020; Dobija et al. 2019; Bollecker 2016). Conversely, when these systems are implemented, motivation is not considered to be affected, since there is the perception that no or very little control is actually exercised (Sutton and Brown 2016). Furthermore, the concept of mindset stands out in strategic management accounting studies, determining how accounting is perceived by each individual, which in turn has an influence on how he/she addresses it (Hutaibat et al. 2011; Hutaibat 2019). However, it is not possible to state whether strategic management accounting increases the performance of HEIs, as knowledge in this area is still limited (Marlina and Tjahjadi 2020). Studies on management control/management control tools allow us to conclude that cultural issues have a great impact on management control practices (see Tsamenyi et al. 2008). More specifically, studies on quality management reveal a lack of acceptance of external evaluation by universities, not only due to cultural and sociotechnical barriers (del Pino et al. 2018), but also because they might not result in major changes for these institutions (Van Kemenade et al. 2008). Our findings also show that although the implementing of a budget is seen as crucial for an HEI that is making changes regarding its management control (Ozdil and Hoque 2017), other factors may restrain such changes (Kenno and Sainty 2017). With regard to studies on sustainability, social responsibility and environmental management, the findings show that the different actors consider information on environmental costs to be useful (Sulaiman and Rahman 2013); however, efforts to improve environmental performance from an accounting point of view are still scarce (Chang 2013). Finally, studies on cost/management accounting, allow us to conclude that HEIs, despite being resistant to this type of change, often end up implementing cost/management accounting, due to external pressures (isomorphic), such as the ones exerted by the government. Consequently, there is sometimes a distortion between the theoretical and real objectives in implementation since these institutions tend to value cost accounting as a means for stakeholder accountability (Brusca et al. 2019).

In short, the findings suggest that despite the importance given to management accounting and control tools in HEIs, several issues such as strategic beliefs, structural autonomy, demographic characteristics, among others, compel these institutions’ different stakeholders to have different perceptions/attitudes towards these instruments, often leading to its partial implementation. Despite this fact, most of the time these institutions end up implementing these instruments due to external pressures.

With regard to the third research question, the findings show that only 15 articles address theories, although 13 different theories were mentioned. The most frequently adopted theory is the institutional theory and its respective approaches: 9 articles address the institutional theory and the isomorphism theory (see Table 1). The findings suggest that most adopted theories have a sociological and psychological nature. This fact is in line with the general literature on management accounting and control (see Scapens 2012; Gong and Tse 2009), which claim that the institutional theory is commonly adopted one (see Al-Htaybat and Alberti-Alhtaybat 2013). Furthermore, 44 articles pertaining to our sample adopted the case study method, something which is stressed in interpretive research (see Jansen 2018). However, case studies are only theoretically generalizable. Therefore, a call for a more positivist approach is needed in order to seek “law-like generalizations” (see Jansen 2018, p. 1489).

Additionally, to better reflect directions for further research themes, our findings were complemented by an analysis of the future research suggested in the articles in the sample. It is important to stress that only 31 (out of 50) studies pointed out future avenues for research in management accounting and control in HEIs. In broader terms, some authors ask for more longitudinal and comparative studies (see, for example, Boitier and Rivière 2013; Heinicke and Guenther 2020; Hutaibat and Alhatabat 2020; Martin-Sardesai 2016). Another set of articles suggests applying their results to other contexts or countries, also extending them to the private sector (see Chung et al. 2009; Broadbent 2010). This is, in part, a consequence of the adoption of the case study method by most studies (44 out of 50).

Consequently, most of them suggest that further research should focus on replicating their case or conducting additional case studies due to reliability and replicability issues. By doing so, best practices could emerge and additional insights can be obtained. Another important avenue for further research would be comparing different education systems, notably with that of the United States of America (US). Although the analyzed articles addressed 46 countries (most of them European), none assessed management accounting and control in US HEIs, and no study addressed African countries. Consequently, future research should assess which management accounting and control tools are adopted in underdeveloped African countries and why. Furthermore, the adoption of quantitative methodologies has been limited and further research should address mixed, experimental and literature methods (see Marlina and Tjahjadi 2020). Additionally, most articles are focused on public HEIs and thus future research should address private ones.

More specifically, according to the main topics which resulted from this SLR, and based on the suggestions made in the articles encompassing the sample, some other reflections on further research were conducted, pointing out different directions (see, for example, Martin-Sardesai et al. 2019; Agyemang and Broadbent 2015; Hutaibat 2019; Hutaibat et al. 2011; Marlina and Tjahjadi 2020; Bobe and Kober 2020; Bollecker 2016; Dobija et al. 2019; Pilonato and Monfardini 2020; Ozdil and Hoque 2017; Arroyo 2017; Wigmore-Álvarez and Ruiz-Lozano 2014), namely:

- Addressing the extent to which negative impacts of performance management systems are due to the dysfunctions resulting from the actions of organizations or individuals. This is an important issue since these impacts may hamper quality research, also leading to rankings which do not truly depict the strength of the HEI;

- Better understanding the complexity of the reactions of academics towards management control systems based in academic rankings. This fact can potentially develop important values, which can be grounded on a more relational approach to management control;

- More empirical evidence is needed to prescribe practical implications to address the obligation to promote a sustainable higher education;

- More studies following the principles of authenticity, plausibility and criticality, mainly in cases where the researcher is a participant observer and a close relationship between him/her and the research subject can be questioned;

- More interpretive research on strategy and accounting in order to develop themes such as strategic costing modeling, accounting competitors and customer accounting. According to Hutaibat et al. (2011), strategic management accounting should be extended to other institutions to obtain a deeper comprehension of the phenomenon;

- Addressing the linkage between HEIs and industry in order to increase HEIS’ performance;

- Better understanding the impact of Deans’ characteristics on the use of MCS and performance measures, since they can greatly affect an HEI’s performance;

- Understanding how the actions undertaken by a presidential team can anticipate or change HEIs’ response to external demands. This is an important matter since stakeholders’ representation may change over time, affecting institutional demands. Consequently, HEIs’ strategic response should adapt to these changes;

- Assessing the impact of international organizations, such as rating and accreditation agencies, regarding the use of performance measures. In fact, several scholars as well as practitioners are still skeptical towards the credibility of those agencies, and consequently towards the use of the proposed measures;

- Assessing the role of other key players such as local authorities, ministries or healthcare organizations. By understanding the role played by these agents, HEIs can gain important insights about how control systems may be improved;

- Assessing the effects of power relations within an HEI, the potential conflicts between agents, as well as the motivational effects. Power exercises within an HEI can both promote collaboration or lead to the emergence of conflicts. Therefore, on the one hand it is crucial for these institutions to know how to overcome potential conflicts and, on the other hand, how to foster collaboration;

- Assessing the effects of innovation and organizational change on HEIs’ budgets. This is an important issue to be explored since changes in an HEI’s internal conditions, dynamics, as well as on the relationships between the different agents, can shape the budget model;

- Assessing the main barriers and drivers of organizational change, something which, for example, can potentially allow HEIs to better assess organizational and contextual factors behind the diversity of roles regarding the campus sustainability;

- Addressing the non-voluntary disclosure of sustainable practices. Nowadays, this is crucial since organizations need to be transparent. Their stakeholders increasingly wish to have a clear vision on how HEIs are managed, not only regarding their economic dimension, but also in relation to their social and environmental dimensions.

Again, it is important to stress that the abovementioned themes not only resulted from suggestions made by various authors pertaining to the sample, but also were not considered and explored in further articles on management accounting and control in HEIs.

Finally, since we living in a “knowledge era” and HEIs use “knowledge” as input and output, it is also suggested that future research should focus on assessing the relationship between management accounting and control and knowledge management and intellectual capital creation in this type of institution. Management accounting and control mechanisms should be adapted to address this reality, in which intangibles resources prevail. Considering the growing importance of organizational sustainability, further research in this area should focus on this theme, namely on issues related to the social and environmental aspects of HEIs. Stakeholders are increasingly valuing social and environmental practices, as well as their disclosure.

This SLR aims to provide a theoretical contribution to research on management accounting and control in higher education institutions and fill the gap in the literature on this specific topic. To do so, several cues for further research were pointed out, such as potential themes to be addressed, different methods to be adopted, or even new countries to serve as new empirical grounds. It also aims to emphasize the importance that both management accounting instruments and management control instruments have in the pursuit of the objectives and management of these institutions, whose mission is central to the development of societies. Regarding practical contributions, this paper may be useful for HEI stakeholders, and for their managers. Through the synthesis of the different studies in this field, it is possible to verify current trends in HEIs with regard to management accounting and control, and apply them in their institutions.

This study is not without limitations. The main one is the use of (only) two databases and the exclusion of publications such as books, conference proceedings and the so-called gray literature, which significantly reduced the sample. Therefore, further research should try to enlarge the sample by including these types of documents.

Author Contributions

Conceptualization, J.A., J.V. and L.A.; methodology, J.V. and J.A.; software, R.S. and C.L.; validation, R.S., L.A. and C.L.; formal analysis, L.A. and J.V.; investigation, J.A., J.V. and L.A.; resources, R.S. and C.L.; data curation, J.A. and J.V.; writing—original draft preparation, J.A., J.V. and L.A.; writing—review and editing, J.V., R.S. and C.L.; supervision, J.V. All authors have read and agreed to the published version of the manuscript.

Funding

The work of the authors Rui Silva and Carmem Leal is supported by national funds, through the FCT—Portuguese Foundation for Science and Technology under the project UIDB/04011/2020. The work of author Rui Silva is also funded by NECE-UBI, Research Centre for Business Sciences, Research Centre and this work are funded by FCT—Fundação para a Ciência e a Tecnologia, IP, project UIDB/04630/2022.

Conflicts of Interest

The authors declare no conflict of interest.

Appendix A

Figure A1.

Themes’ evolution over time.

References

- Abba, Magaji, Lawan Yahaya, and Naziru Suleiman. 2018. Explored and Critique of Contingency Theory for Management Accounting Research. Journal of Accounting and Financial Management 4: 40–50. [Google Scholar]

- Acevedo, Rafael A., José María Rueda Rincón, and Neley Arcely Rueda. 2014. Contabilidad Gerencial y Toma de Decisiones Emergentes En La Universidad Politécnica Territorial Andrés Eloy Blanco de Barquisimeto, Estado Lara: Un Análisis Fenomenológico. Visión Gerencial 1: 7–26. [Google Scholar]

- Agasisti, Tommaso, Michela Arnaboldi, and Giovanni Azzone. 2008. Strategic Management Accounting in Universities: The Italian Experience. Higher Education 55: 1–15. [Google Scholar] [CrossRef]

- Agyemang, Gloria, and Jane Broadbent. 2015. Management Control Systems and Research Management in Universities: An Empirical and Conceptual Exploration. Accounting, Auditing & Accountability Journal 28: 1018–46. [Google Scholar]

- Ahrens, Thomas, and Rihab Khalifa. 2015. The Impact of Regulation on Management Control: Compliance as a Strategic Response to Institutional Logics of University Accreditation. Qualitative Research in Accounting & Management 12: 106–26. [Google Scholar]

- Al-Htaybat, Khaldoon, and Larissa von Alberti-Alhtaybat. 2013. Management accounting theory revisited: Seeking to increase research relevance. International Journal of Business and Management 8: 12. [Google Scholar]

- Arroyo, Paulina. 2017. A New Taxonomy for Examining the Multi-Role of Campus Sustainability Assessments in Organizational Change. Journal of Cleaner Production 140: 1763–74. [Google Scholar] [CrossRef]

- Bobe, Belete J., and Ralph Kober. 2020. University Dean Personal Characteristics and Use of Management Control Systems and Performance Measures. Studies in Higher Education 45: 235–57. [Google Scholar] [CrossRef]

- Boitier, Marie, and Anne Rivière. 2013. Freedom and Responsibility for French Universities: From Global Steering to Local Management. Accounting, Auditing & Accountability Journal 26: 616–49. [Google Scholar]

- Boitier, Marie, and Anne Rivière. 2016. Management Control Systems, Vectors of a Managerial Logic: Institutional Change and Conflicts of Logics at University. Comptabilite-Controle-Audit 22: 47–79. [Google Scholar] [CrossRef]

- Bollecker, Marc. 2016. The Adoption of Management Accounting at University: The Presence of Internal Cleavages in a Contradictory Institutional Demands Context. Accounting Auditing Control 22: 109–38. [Google Scholar]

- Broadbent, Jane. 2010. The UK Research Assessment Exercise: Performance Measurement and Resource Allocation. Australian Accounting Review 20: 14–23. [Google Scholar] [CrossRef]

- Brusca, Isabel, Margarita Labrador, and Vicente Condor. 2019. Management Accounting Innovations in Universities: A Tool for Decision Making or for Negotiation? Public Performance & Management Review 42: 1138–63. [Google Scholar]

- Chang, Huei-Chun. 2013. Environmental Management Accounting in the Taiwanese Higher Education Sector: Issues and Opportunities. International Journal of Sustainability in Higher Education 14: 133–45. [Google Scholar] [CrossRef]

- Chung, Tze Ki Jennie, Graeme L. Harrison, and Robert C. Reeve. 2009. Interdependencies in Organization Design: A Test in Universities. Journal of Management Accounting Research 21: 55–73. [Google Scholar] [CrossRef]

- Dobija, Dorota, Anna Maria Górska, Giuseppe Grossi, and Wojciech Strzelczyk. 2019. Rational and Symbolic Uses of Performance Measurement: Experiences from Polish Universities. Accounting, Auditing & Accountability Journal 32: 750–81. [Google Scholar]

- del Pino, Eulalia María, Ramón Murguía, and José Motenegro. 2018. Application of a diagnostic methodology for the change of organizational culture in higher education institutions. Revista Espacios 39: 1–9. [Google Scholar]

- El Filali, Yasmine Benabdelkrim, and Mohammed Saber Hassainate. 2018. The Contribution of Management Control to the Improvement of University Performance. Journal of North African Research in Business 2018: 842469. [Google Scholar] [CrossRef]

- Funck, Elin K., and Tom S. Karlsson. 2020. Twenty—five years of studying new public management in public administration: Accomplishments and limitations. Financial Accountability & Management 36: 347–75. [Google Scholar]

- Gong, Maleen Z., and Michael S. C. Tse. 2009. Pick, Mix or Match? A Discussion of Theories for Management Accounting Research. JABM: Journal of Accounting Business and Management 16: 54–66. [Google Scholar]

- Guenther, Thomas W., and Ulrike Schmidt. 2015. Adoption and Use of Management Controls in Higher Education Institutions. In Incentives and Performance. Berlin: Springer, pp. 361–78. [Google Scholar]

- Habersam, Michael, Martin Piber, and Matti Skoog. 2013. Knowledge Balance Sheets in Austrian Universities: The Implementation, Use, and Re-Shaping of Measurement and Management Practices. Critical Perspectives on Accounting 24: 319–37. [Google Scholar] [CrossRef]

- Hardan, Abdullah Salah, and Tareq Mohd Shatnawi. 2013. Impact of Applying the ABC on Improving the Financial Performance in Telecom Companies. International Journal of Business and Management 8: 48. [Google Scholar] [CrossRef] [Green Version]

- Heinicke, Xaver, and Thomas W. Guenther. 2020. The Role of Management Controls in the Higher Education Sector: An Investigation of Different Perceptions. European Accounting Review 29: 581–630. [Google Scholar] [CrossRef]

- Hiebl, Martin R. W. 2014. Upper Echelons Theory in management accounting and control Research. Journal of Management Control 24: 223–40. [Google Scholar] [CrossRef]

- Huerta-Riveros, Patricia C., Héctor G. Gaete-Feres, and Liliana M. Pedraja-Rejas. 2020. Dirección Estratégica, Sistema de Información y Calidad. El Caso de Una Universidad Estatal Chilena. Información Tecnológica 31: 253–66. [Google Scholar] [CrossRef]

- Hutaibat, Khaled. 2019. Accounting for Strategic Management, Strategising and Power Structures in the Jordanian Higher Education Sector. Journal of Accounting& Organizational Change 15: 430–52. [Google Scholar]

- Hutaibat, Khaled, and Zaidoon Alhatabat. 2020. Management Accounting Practices’ Adoption in UK Universities. Journal of Further and Higher Education 44: 1024–38. [Google Scholar] [CrossRef]

- Hutaibat, Khaled, Larissa von Alberti-Alhtaybat, and Khaldoon Al-Htaybat. 2011. Strategic Management Accounting and the Strategising Mindset in an English Higher Education Institutional Context. Journal of Accounting & Organizational Change 7: 358–90. [Google Scholar]

- Jacomossi, Fellipe Andre, and Marcia Zanievicz da Silva. 2016. Influence of Environmental Uncertainty in the Use of Management Control System in a Higher Education Institution/Influencia Da Incerteza Ambiental Na Utilizacao de Sistemas de Controle Gerencial Em Uma Instituicao de Ensino Superior. Revista de Gestao USP 23: 75–86. [Google Scholar] [CrossRef] [Green Version]

- Jansen, E. Pieter. 2018. Bridging the gap between theory and practice in management accounting: Reviewing the literature to shape interventions. Accounting, Auditing & Accountability Journal 31: 1486–509. [Google Scholar]

- Jiang, Darong. 2019. Management Accounting Literature Review—Based on the Development of Management Accounting Research in 2015–17. Modern Economy 10: 2315–34. [Google Scholar] [CrossRef] [Green Version]

- Johnson, H. Thomas, and Robert S. Kaplan. 1987. The Rise and Fall of Management Accounting. IEEE Engineering Management Review 15: 36–44. [Google Scholar] [CrossRef]

- Jones, Larry R., Fred Thompson, and William Zumeta. 1986. Reform of Budget Control in Higher Education. Economics of Education Review 5: 147–58. [Google Scholar] [CrossRef]

- Jovanović, Tatjana, and Martina Dragija. 2018. Application of the Accounting Information at Higher Education Institutions in Slovenia and Croatia-Preparation of Public Policy Framework. International Journal of Public Sector Performance Management 4: 452–66. [Google Scholar] [CrossRef]

- Kallio, Tomi J., Kirsi-Mari Kallio, and Annika Blomberg. 2020. From Professional Bureaucracy to Competitive Bureaucracy--Redefining Universities’ Organization Principles, Performance Measurement Criteria, and Reason for Being. Qualitative Research in Accounting & Management 17: 82–108. [Google Scholar]

- Kenno, Staci A., and Barbara Sainty. 2017. Revising the Budgeting Model: Challenges of Implementation at a University. Journal of Applied Accounting Research 18: 496–510. [Google Scholar] [CrossRef]

- Kont, Kate-Riin, and Signe Jantson. 2011. Activity-Based Costing (ABC) and Time-Driven Activity-Based Costing (TDABC): Applicable Methods for University Libraries? Evidence Based Library and Information Practice 6: 107–19. [Google Scholar] [CrossRef] [Green Version]

- Küpper, Hans-Ulrich. 2013. A Specific Accounting Approach for Public Universities. Journal of Business Economics 83: 805–29. [Google Scholar] [CrossRef]

- Laitinen, Erkki K. 2003. Future-Based Management Accounting: A New Approach with Survey Evidence. Critical Perspectives on Accounting 14: 293–323. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas G. Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter C. Gøtzsche, John P. A. Ioannidis, Mike Clarke, P. J. Devereaux, Jos Kleijnen, and David Moher. 2009. The PRISMA Statement for Reporting Systematic Reviews and Meta-Analyses of Studies That Evaluate Health Care Interventions: Explanation and Elaboration. Journal of Clinical Epidemiology 62: e1–34. [Google Scholar] [CrossRef] [Green Version]

- Marlina, Evi, and Bambang Tjahjadi. 2020. Strategic management accounting and university performance: A critical review. Academy of Strategic Management Journal 19: 1–5. [Google Scholar]

- Marlina, Evi, Hendri Ali Ardi, Siti Samsiah, Kirmizi Ritonga, and Amris Rusli Tanjung. 2020. Strategic Costing Models as Strategic Management Accountin Techniques at Private Universities in Riau, Indonesia. International Journal of Financial Research 11: 274–83. [Google Scholar] [CrossRef]

- Martin-Sardesai, Ann. 2016. Institutional Entrepreneurship and Management Control Systems. Pacific Accounting Review 28: 458–70. [Google Scholar] [CrossRef]

- Martin-Sardesai, Ann, James Guthrie, Stuart Tooley, and Sally Chaplin. 2019. History of Research Performance Measurement Systems in the Australian Higher Education Sector. Accounting History 24: 40–61. [Google Scholar] [CrossRef]

- Minelli, Eliana, Gianfranco Rebora, and Matteo Turri. 2015. Quest for Accountability: Exploring the Evaluation Process of Universities. Quality in Higher Education 21: 103–31. [Google Scholar] [CrossRef]

- Modell, Sven. 2006. Institutional and Negotiated Order Perspectives on Cost Allocations: The Case of the Swedish University Sector. European Accounting Review 15: 219–51. [Google Scholar] [CrossRef]

- Molina-Sanchez, Horacio, Antonio Ariza-Montes, Mar Ortiz-Gomez, and Antonio Leal-Rodriguez. 2019. The Subjective Well-Being Challenge in the Accounting Profession: The Role of Job Resources. International Journal of Environmental Research and Public Health 16: 3073. [Google Scholar] [CrossRef] [Green Version]

- Ozdil, Esin, and Zahirul Hoque. 2017. Budgetary Change at a University: A Narrative Inquiry. The British Accounting Review 49: 316–28. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, Elie A. Akl, Sue E. Brennan, and et al. 2021. The PRISMA 2020 Statement: An Updated Guideline for Reporting Systematic Reviews. BMJ 372: 1–9. [Google Scholar] [CrossRef]

- Palowski, Henry T. 2011. Misinterpretation of the Strategic Significance of Cost Driver Analysis: Evidence from Management Accounting Theory and Practice. Ekonomika Regiona 2: 131. [Google Scholar] [CrossRef]

- Pelz, Michael. 2019. Can management accounting Be helpful for young and small companies? Systematic review of a paradox. International Journal of Management Reviews 21: 256–74. [Google Scholar] [CrossRef]

- Petrides, Lisa A., Sara I. McClelland, and Thad R. Nodine. 2004. Costs and Benefits of the Workaround: Inventive Solution or Costly Alternative. International Journal of Educational Management 18: 100–8. [Google Scholar] [CrossRef] [Green Version]

- Pilonato, Silvia, and Patrizio Monfardini. 2020. Performance Measurement Systems in Higher Education: How Levers of Control Reveal the Ambiguities of Reforms. The British Accounting Review 52: 100908. [Google Scholar] [CrossRef]

- Rashid, Tayyab, and Robert McGrath. 2020. Strengths-Based Actions to Enhance Wellbeing in the Time of COVID-19. International Journal of Wellbeing 10: 113–32. [Google Scholar] [CrossRef]

- Sánchez, Rosario del Río, Vanessa Rodriguez Cornejo, Teresa García-Valderrama, and Jaime Sanchez-Ortiz. 2019. Design of the activities map with the ABC cost model for the university departments. Cuadernos de Gestion 19: 159–84. [Google Scholar] [CrossRef] [Green Version]

- Scapens, Robert W. 2012. Institutional Theory and Management Accounting Research. Maandblad Voor Accountancy En Bedrijfseconomie 86: 401. [Google Scholar] [CrossRef] [Green Version]

- Schaltegger, Stefan, and Dimitar Zvezdov. 2015. Gatekeepers of Sustainability Information: Exploring the Roles of Accountants. Journal of Accounting and Organizational Change 11: 333. [Google Scholar] [CrossRef]

- Shields, Michael D. 2018. A Perspective on Management Accounting Research. Journal of Management Accounting Research 30: 1–11. [Google Scholar] [CrossRef]

- Sizer, John. 1981. Performance Assessment in Institutions of Higher Education under Conditions of Financial Stringency, Contraction and Changing Needs: A Management Accounting Perspective. Accounting and Business Research 11: 227–42. [Google Scholar] [CrossRef]

- Sulaiman, Maliah, and Noredah Abdul Rahman. 2013. Does the Environment Matter? Empirical Evidence from an Institution of Higher Learning in Malaysia. International Journal of Business & Society 14: 177–92. [Google Scholar]

- Sutton, Nicole C., and David A. Brown. 2016. The Illusion of No Control: Management Control Systems Facilitating Autonomous Motivation in University Research. Accounting & Finance 56: 577–604. [Google Scholar]

- Tranfield, David, David Denyer, and Palminder Smart. 2003. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review*. British Journal of Management 14: 207–22. [Google Scholar] [CrossRef]

- Tsamenyi, Mathew, Irvan Noormansyah, and Shahzad Uddin. 2008. Management Controls in Family-Owned Businesses (FOBs): A Case Study of an Indonesian Family-Owned University. Accounting Forum 32: 62–74. [Google Scholar] [CrossRef] [Green Version]

- Van Kemenade, Everard, Mike Pupius, and Teun W Hardjono. 2008. More Value to Defining Quality. Quality in Higher Education 14: 175–85. [Google Scholar] [CrossRef]

- Visser, Max. 2016. Management Control, Accountability, and Learning in Public Sector Organizations: A Critical Analysis. In Governance and Performance in Public and Non-Profit Organizations. Bingley: Emerald Group Publishing Limited. [Google Scholar]

- Wigmore-Álvarez, Amber, and Mercedes Ruiz-Lozano. 2014. The United Nations Global Compact Progress Reports as Management Control Instruments for Social Responsibility at Spanish Universities. Sage Open 4. [Google Scholar] [CrossRef]

- Yakhou, Mehenna, and Kevin Ulshafer. 2012. Adapting the Balanced Scorecard and Activity-Based Costing to Higher Education Institutions. International Journal of Management in Education 6: 258–72. [Google Scholar] [CrossRef]